In the past 2022, the domestic chemical product market has shown a rational decline as a whole. According to statistics from business clubs, 64%of the 106 mainstream chemical products monitored in 2022, 64%of products fell, 36%of products rose. The chemical products market showed rising new energy categories, decline in traditional chemical products, stabilizing basic raw materials The pattern. In the series of “Review of the 2022 Chemical Market” series launched in this edition, it will be selected the top rising and falling products for analysis.

2022 is undoubtedly a high time in the lithium salt market. Lithium hydroxide, lithium carbonate, lithium iron phosphate, and phosphate ore occupied the top 4 seats in the increase list of chemical products, respectively. In particular, the lithium hydroxide market, the main melody of the strong rising and high sideways throughout the year, eventually topped the list of 155.38% annual increase.

Two rounds of strong pull rising and innovative high

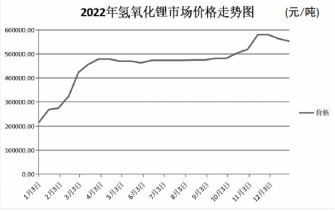

The trend of lithium hydroxide market in 2022 can be divided into three stages. In early 2022, the lithium hydroxide market opened the market at a average price of 216,700 yuan (ton price, the same below). After the strong rise in the first quarter, it maintained a high level in the second and third quarters. The average price of 10,000 yuan was ended, and the year increased by 155.38%

In the first quarter of 2022, the quarterly increase in the lithium hydroxide market reached 110.77%, of which in February increased to the largest year, reaching 52.73%. According to statistics from business clubs, at this stage, it is supported by upstream ore, and the price of lithium lithium carbonate has continued to support lithium hydroxide. At the same time, due to tight raw materials, the overall operating rate of lithium hydroxide fell to about 60 %, and the supply surface was tight. The demand for lithium hydroxide in downstream high -nickel ternary battery manufacturers has increased, and the mismatch of supply and demand has promoted the strong rise in the price of lithium hydroxide.

In the second and third quarters of 2022, the lithium hydroxide market showed a high volatile trend, and the average price rose slightly by 0.63%in this cycle. From April to May of 2022, lithium carbonate was weakened. Some of the new capacity of some lithium hydroxide manufacturers released, the overall supply increase, the demand for domestic downstream spot procurement has slowed down, and the lithium hydroxide market appeared high. Beginning in June 2022, the price of lithium carbonate was raised slightly to support the market conditions of lithium hydroxide, while the enthusiasm of the downstream inquiry was slightly improved. It reached 481,700 yuan.

Entering the fourth quarter of 2022, the lithium hydroxide market rose again, with a quarterly increase of 14.88%. In the peak season atmosphere, the production and sales of new energy vehicles in the terminal have increased significantly, and the market is difficult to find. The superimposed new energy subsidy policy is approaching at the end of the end, and some car companies will prepare in advance to drive the lithium hydroxide market for strong demand for energy batteries. At the same time, affected by the domestic epidemic, the spot supply of the market is tight, and the lithium hydroxide market will rise again. After mid -November 2022, the price of lithium carbonate declined, and the lithium hydroxide market fell slightly, and the final price closed at 553,300 yuan.

The supply of upstream raw materials is tight supply

Looking back at 2022, not only the lithium hydroxide market rose like a rainbow, but the other lithium salt series products performed brightly. Lithium carbonate rose 89.47%, lithium iron phosphate increased annual increases of 58.1%, and the annual increase of the upstream phosphorus ore of lithium iron phosphate also reached 53.94%. Essence The industry believes that the main reason for the skyrocketing lithium salt in 2022 is that the cost of lithium resources continues to rise, which has led to the continuous increase in the shortage of lithium salt supply, thereby pushing the price of lithium salt.

According to a new energy battery marketing personnel in Liaoning, lithium hydroxide is mainly divided into two production routes of lithium hydroxide and salt lake preparing for lithium hydroxide and salt lake. Lithium hydroxide after industrial -grade lithium carbonate. In 2022, enterprises using lithium hydroxide using pylori were subject to tight mineral resources. On the one hand, lithium hydroxide production capacity is limited under the lack of lithium resources. On the other hand, there are currently a handful of lithium hydroxide producers certified by international battery faucet, so the supply of high -end lithium hydroxide is more limited.

Ping An Securities analyst Chen Xiao pointed out in the research report that the problem of raw materials is an important disturbance factor for the lithium battery industry chain. For salt lake brine lithium lifting routes, due to the cooling of the weather, the evaporation of salt lakes decreases, and the supply has a shortage of supply, especially in the first and fourth quarters. Due to the scarce resource attributes of lithium iron phosphate, due to the scarce resource attributes, the spot supply was insufficient and promoted the high level of operation, and the annual increase reached 53.94%.

Terminal new energy demand increased

As a key raw material for high -nickel ternary lithium -ion batteries, the strong growth of the demand for downstream new energy vehicle industries has provided source motivation than the rise in lithium hydroxide prices.

Ping An Securities pointed out that the new energy terminal market continued to be strong in 2022, and its performance was still dazzling. The production of downstream battery factories in lithium hydroxide is active, and the demand for high nickel ternary batteries and iron lithium continues to improve. According to the latest data from the China Automobile Association, from January to November 2022, the production and sales of new energy vehicles were 6.253 million and 60.67 million, respectively, a average year -on -year increase, and the market share reached 25%.

In the context of resource shortage and strong demand, the price of lithium salts such as lithium hydroxide has soared, and the lithium electricity industry chain has fallen into “anxiety”. Both power battery material suppliers, manufacturers and new energy automobile manufacturers are stepping up their buying of lithium salts. In 2022, several battery material manufacturers signed supply contracts with lithium hydroxide suppliers. A wholly-owned subsidiary of Avchem Group signed a supply contract for battery grade lithium hydroxide with Axix. It has also signed contracts with Tianhua Super Clean’s subsidiary Tianyi Lithium and Sichuan Tianhua for battery-grade lithium hydroxide products.

In addition to battery companies, car companies are also actively competing for lithium hydroxide supplies. In 2022, it is reported that Mercedes-Benz, BMW, General Motors and other automobile companies have signed supply agreements for battery grade lithium hydroxide, and Tesla also said that it would build a battery grade lithium hydroxide chemical plant, directly entering the field of lithium chemical production.

On the whole, the booming development prospect of the new energy automobile industry has brought huge market demand for lithium hydroxide, and the shortage of upstream lithium resources has led to the limited production capacity of lithium hydroxide, pushing its market price to a high level.

Post time: Feb-02-2023